Originally published in The Actuary in September 2020.

https://www.theactuary.com/features/2020/09/02/prepare-impact-covid-19

On 11 March 2020, the World Health Organisation declaredCovid-19 a pandemic. Since then, most of the world has been in some form of lockdown (UK: 23 March), from which some have only now begun to emerge. At the point of writing, the number of cases worldwide exceeds 13m, with almost 600,000 deaths[1]. Official statistics indicate UK Covid-19 deaths are over 50,000[2], with excess deaths at 62,500 at 26 June[3]. Both the pandemic and its economic impacts, which we consider here, are far from over.

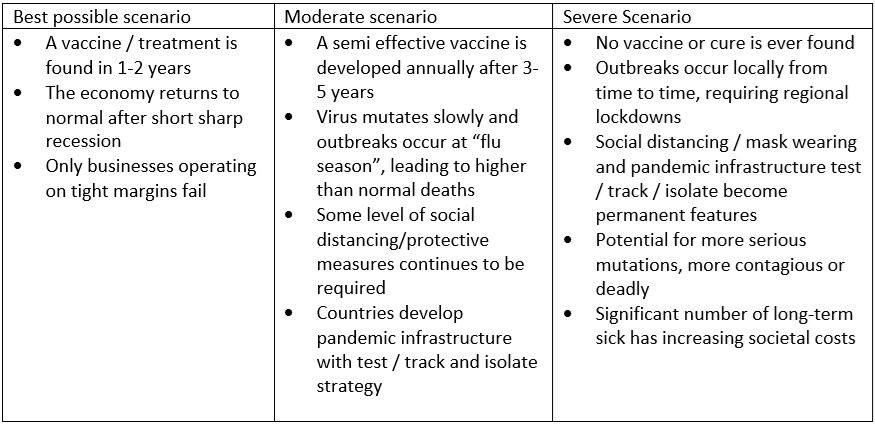

The extent of the economic impact will depend on how long Covid-19impacts last and countries’ economic outlook before the pandemic. In particular, in the UK, outcomes will likely be exacerbated by the economic impacts of Brexit. Three scenarios below emphasize a plausible range of outcomes.

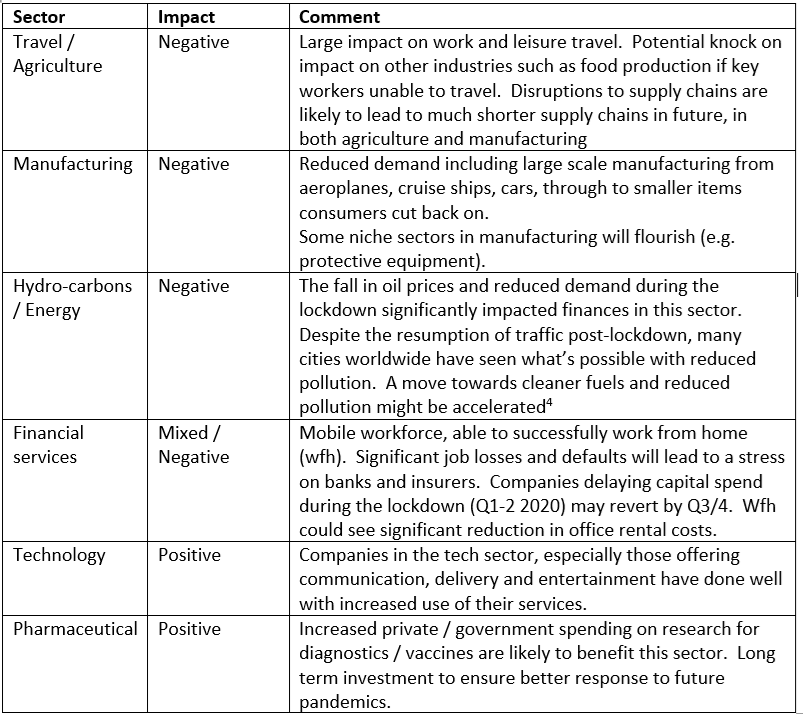

Under the moderate / severe scenarios, the impact on specific business sectors could be as described in the table below.

Unemployment and re-purposing of labour: One reason that pandemics lead to depressed real interest rates is a re-prioritisation of labour versus capital [5]. However, compared to historic pandemics, lockdowns have so far limited the loss of life (0.5 million), compared to Spanish Flu (100 million) or Black Death (75million). The mortality impact disproportionately affects older people who are less likely to be actively in the work force.

Job losses as a result of the virus and lockdown on the sectors above could significantly impact the economy. So far, this impact has been ameliorated by the governments’ generous “furlough” schemes. Consumer spending, already reduced, will reduce further as support schemes end.

Capital cities’ existential crisis? Social disorder, cost of property and small apartment sizes, may make metropolitan cities less attractive. Smaller, greener, less expensive towns may do better. In particular, London’s relatively poor digital infrastructure, high living costs, reduced attractions(restaurants, night life) and a likely messy Brexit could permanently reduce its attractiveness as a financial centre.

The pandemic will impact people depending entirely on whether they can work from home.

Overall private indebtedness has fallen[6], while lending to businesses has increased significantly[7]. The additional debt strain on companies’ balance sheets could lead to a wave of defaults in 2021

The spending necessary to ease the pain of the lockdown increased government indebtedness, which, at May 2020, exceeded GDP for the first time since 1963[8]. In addition, the government has acted as guarantor of approximately 80% of commercial loans on various Coronavirus Schemes – Coronavirus Business Interruption Loan Scheme (CBILS), Coronavirus Large Business Interruption Loan Scheme (CLBILS) and the Bounce Back Loan Scheme (BBLS)[9].

Six tools that governments / central banks could use post-Covid are below:

The UK base rate is at 0.1% (1 July 2020). There is limited scope to reduce rates further. The equivalent base rate is already negative in some countries (Denmark, Japan, Sweden and Switzerland) and the EU. A negative base rate means commercial bank spay the Bank to hold reserves and excess cash. This penalises banks for holding cash at the central bank, encouraging lending to businesses. Low interest rates should encourage borrowing for capital investment, although firms may not consider this the right time for such investment. A move to digital[10] currencies would make negative interest rates easier to implement in practice.

The Bank can increase the supply of money in the economy through purchasing assets (gilts, corporate bonds) on the open market or engage in repo trades / secured lending with commercial banks. The impacts of purchasing government bonds would usually be to:

· Lower the risk-free rate (through increased price of government bonds), thus reducing government / corporate cost of borrowing

· Increase the supply of money in the economy through quantitative easing (QE)

· Be a source of direct government funding

This may not have the intended effect. Many commercial banks lack confidence in the economy and are not freely lending, preferring to keep excess reserves at the central banks, despite low or negative interest rates. The rapid increase in excess reserves held at central banks [11] has ensured that QE has had little inflationary effect on the prices of goods and services, although it has led to asset inflation. The lack of price inflation has not reduced the value of government debt in real terms.

Purchasing corporate bonds will similarly increase money supply (to holders of those bonds). This would lower corporate spreads relative to base rate, assisting indebted companies seeking to re-borrow directly. Depending on targeted purchases, this could also remove poor-quality, deflationary assets (e.g. US “junk” bonds) from the commercial market. This option may be unpopular, perceived as yet another bail out of hedge funds either holding these junk bonds or who have shorted longer term corporate bonds.

A co-ordinated move to convert government debt to undated redemption dates[12] would avoid governments having to roll over debts on potentially unfavourable terms, and effectively amount to a soft default. This would have large implications for the insurance industry where available assets for matching purposes would decline significantly.

By reducing social spending, the government can use its revenue to reduce debt levels, with the hope of reducing debt as a proportion of GDP. However, following almost a decade of austerity in the UK, it is unlikely that the government can continue to cut without damaging the fabric of society, by reducing the incomes and benefits of those who need it the most and further depleting the “essential” services (teachers, transport, NHS workers) that the country relies on.

This could further reduce confidence as many of those whose spending might otherwise stimulate the economy will now find discretionary spending difficult, particularly once the furlough scheme ends 9. A knock-on impact could be reduced GDP, resulting in deflation and defaults.

The government has urged banks to keep lending channels open. Defaults are likely from companies with low margins and specific sectors heavily impacted by the virus. There is likely to be some “junking” of corporate bonds and non-repayment of loans. Should government step in?

Government intervention could stop further contamination or loss of confidence in the economy. Despite the overall similarity between par values of corporate bonds and bank loans, corporate default crises on their own have less of a real impact on the economy than banking crises[13]. Large corporations (typical issuers of corporate bonds) have other avenues for raising capital. Currently, the pandemic hasn’t caused a banking crisis or affected all sectors evenly. Following years of austerity and recent financial sector bailouts, this would be a highly unpopular move. Given high levels of government borrowing and the desire to recoup costs through taxes, this seems an unlikely avenue.

However, large scale corporate bond defaults that begin to lead to contagion in the banking sector could change matters. Bail in regulations have already been enacted so that shareholders and creditors would share in the pain of resolving a bank failure, rather than the taxpayer bailouts in the 2008financial crisis.

In 2008, the UK government nationalised Northern Rock, HBOS, Lloyd’s TSB and RBS [14]. Merrill Lynch, Freddie Mac, Fannie Mae and AIG were bailed out by the US government. Nationalisation was used to avoid systemic risk from bank insolvencies and may be required again including for insurance companies.

Nationalisation has complications. It socialises the losses of private companies that have taken profits over recent years and raises the question as to which industries are deemed essential. So far, the financial sector has managed the pandemic reasonably well. There is, as yet, no reason to nationalise or bail out banks or insurance companies.

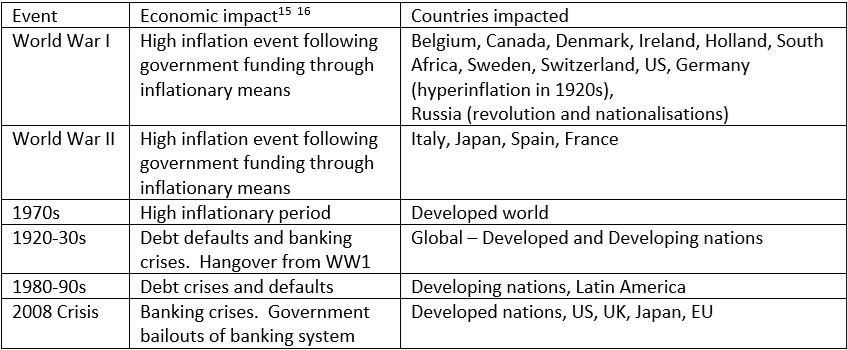

The economic impact of this pandemic will depend on its path and government actions. Significant recent inflationary and default periods are highlighted below.

Pandemics (including recent ones of 1957 and 1968) have not had economic impacts as serious as events above.

Preparation for defaults, downgrades and inflation

While the eventual economic path is still uncertain, insurers can prepare for various possible outcomes, for example by rebalancing corporate bond, property and equity exposures to avoid exposed sectors or ensuring adequate protection from inflation risk.

The impact on insurers’ balance sheets due to changed mortality is far from clear. An increase in existing annuitants’ mortality could reverse some of the recent improvements, releasing capital. The impact on projected longevity is less clear, with a possibly healthier cohort remaining post Covid with impacts on long term sick largely unknown.

While the economic impact on most of the insured population is unlikely to be severe, a fall in economic confidence overall could impact new business sales. The impact will differ by product group, with protection likely to fare better than savings products. There could be significant consequences for expenses.

Depressed yields and possible defaults could negatively affect annuitant portfolios, particularly matching adjustment business. On investment portfolios, there may be continued depressed profits from fund margins due to lower asset values.

Reconsideration of pandemic and other risks

In insurance, being an outlier can cause products to be uncompetitive or attract the unwelcome attentions of the regulator. As a result, many aspects of insurers’ models and solutions converge. Over reliance on the 1918 Spanish flu as the pandemic scenario and the lack of consideration of other available information left us unprepared.

While capital held for pandemic risk is likely, in most cases, to have been appropriate, the interaction with other risks (e.g. correlation with market, operational risk) was not appropriately allowed for. A key question now is whether there are similar oversights with other insurance risks.

Is capital the right way to protect against systemic risk?

For any globally systemic risk, is holding capital an effective means of protection? Or put another way, are we so reliant on the substantial amount of capital held under Solvency II regulation that we fail to consider issues that cannot be solved by capital?

Collaboration and pooling of risk across companies, governments or regions could be considered to prepare against systemic risks that are crystallising. Could funds accrued through premium levies such as the Financial Services Compensation Scheme be made available in exceptional circumstances such as this?

Revised company scenarios reflecting actions and plans not for a single risk but for connected risk should be considered and published.

With the pandemic itself, early action was the correct approach, with indecisiveness heavily punished with large excess deaths and economic damage. Insurance companies will need to be pro-active to ensure they manage emerging risks to avoid the worst scenarios.

[1] https://www.worldometers.info/coronavirus/#countries

[2] https://www.ons.gov.uk/peoplepopulationandcommunity/healthandsocialcare/conditionsanddiseases/articles/coronaviruscovid19roundup/2020-03-26#coviddeaths

[3] https://www.actuaries.org.uk/system/files/field/document/Mortality-monitor-Week-26-2020-v01-2020-07-07.pdf

[4] https://www.ft.com/content/590b1fec-af0d-11ea-a4b6-31f1eedf762e

[5] The long economic hangover of pandemics, Jorda, Singh and Taylor, 2020, https://www.imf.org/external/pubs/ft/fandd/2020/06/long-term-economic-impact-of-pandemics-jorda.htm

[6] https://www.bankofengland.co.uk/statistics/money-and-credit/2020/may-2020

[7] https://www.ons.gov.uk/economy/grossdomesticproductgdp/timeseries/dgd8/ukea

[8] https://www.ons.gov.uk/economy/governmentpublicsectorandtaxes/publicsectorfinance,Public Sector Finances, UK: May 2020

[9] (Coronavirus: Effect on the Economy, Commons Library Briefing, 19 June 2020)

[10] https://www.riksbank.se/en-gb/payments--cash/e-krona/

[11] https://fred.stlouisfed.org/series/EXCSRESNS

[12] https://www.sttk.fi/en/2020/04/22/perpetual-bonds-and-other-means-of-cancelling-government-debts/

[13] Macroeconomic Effects of Corporate Default Crises: A long term perspective, Giesecke, Longstaff, Schaefer, Strebulaev, February 2012, https://www.nber.org/papers/w17854

[14] https://www.theguardian.com/business/2008/dec/28/markets-credit-crunch-banking-2008#:~:text=Not%20since%201929%20has%20the,and%20had%20to%20be%20rescued.

[15] Dimson, Marsh, Staunton “Triumph of the Optimists” P66

[16] Sovereign-debt relief and its aftermath: The 1930s, the 1990s, thefuture? Carmen Reinhart, Christoph Trebesch 21 October 2014 https://voxeu.org/article/sovereign-debt-relief-and-its-aftermath-1930s-1990s-future